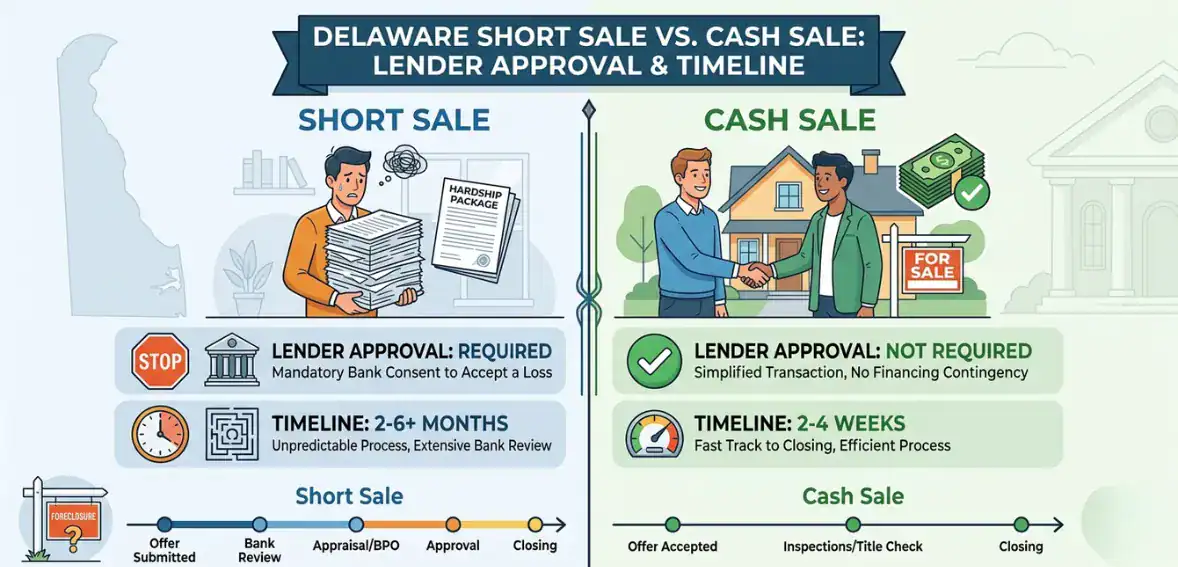

When buying or selling a home in Delaware, understanding the Delaware short sale timeline is crucial. Unlike a cash sale, a short sale requires lender approval because the sale proceeds are less than the mortgage balance. This additional step adds time to the process, while cash sales typically close much faster since no lender review or approval is needed.

What Is a Short Sale?

A short sale is a property sale where the owner sells the home for less than what is still owed on the mortgage. In such situations, the bank has to agree to the sale since the sale proceeds will be less than the remaining loan amount. Most of the time, short sales are done as a last resort by homeowners facing financial hardship who are unable to keep up with their mortgage payments but want to avoid their house being foreclosed. After the lender considers the seller’s letter of explanation, income documents, and a net sheet depicting the shortfall, it usually agrees to the reduced payoff.

What Is a Long-Term

A cash sale means the buyer of a property hands over the entire purchase price at the time of the agreement in cash or cash equivalents, without seeking a mortgage or loan. Since the buyer is bringing in sufficient funds to take care of all existing mortgages, liens, and closing costs, the borrower will not have to get the lender’s approval. Generally, processing cash sales takes less time and is simpler than paper-based transactions. They often close in 2-4 weeks with relatively fewer hassle, paperwork, and risk of delays, which makes them a preferred choice for both buyers and sellers looking for a quick and easy sale.

Delaware Short Sale vs. Cash Sale: What Sets a Delaware Short Sale apart?

In Delaware, a short sale is quite different from a cash sale, mainly because of the lender’s involvement and how the proceeds are handled. If it is a short sale, the lender has to give their approval because you are selling the property at a price lower than your mortgage, hence the bank has to first check the offer, then go through a hardship package, and finally approve the net proceeds before the sale can be closed.

The approval process, which usually features several lien holders and thorough financial documentation, is the main reason that short sales take much longer than regular sales; in fact, they can take anywhere from 60 to 120 days or more to be completed.

Therefore, cash sales tend to be very fast and simple, usually closing within just a few weeks, because without a lender, there is no need to negotiate, there is no requirement for hardship documentation, and there is no lengthy review process. This shows why things like time, complexity, and procedural requirements are so different between the two types of real estate transactions in Delaware.

Lender Requirements for a Delaware Short Sale

Hardship Documentation

Lenders require homeowners to submit a hardship package explaining the reason for their inability to continue making mortgage payments. Typically, this involves a comprehensive letter detailing financial struggles, for example, unemployment, sudden medical expenses, divorce, or other emergencies.

Besides the letter, you will have to provide your income documentation, such as recent pay stubs, tax returns, and bank statements, to reveal your current financial status. Lenders also require a breakdown of your monthly expenses to comprehend the reason why making payments is not a viable option. This is helpful to them to not only grasp your situation but also to decide whether a short sale is appropriate.

Mortgage Statement

A mortgage statement is a crucial document for demonstrating to the lender the amount of your mortgage balance left. A short sale lender will use the mortgage statement to determine the amount of the mortgage balance outstanding, and from there, the amount that may have to be written off, in case of approval of the short sale.

Giving a correct and up-to-date mortgage statement can expedite the approval process and make sure that all the numbers are clear and verified.

Financial Overview (Net Sheet)

A net sheet is an itemized financial breakdown that lays out the comparison between the anticipated house sale proceeds and the remaining mortgage and other expenses. It will list down the intended sale price, total mortgage balance, other liens, estimated closing costs, and the deficit the lender will have to absorb.

Furthermore, lenders get a comparative market analysis (CMA) or an appraisal to make sure that the selling price is the fair market value of the house. This not only confirms that the sale is reasonable to the lender but also that it complies with the loss mitigation guidelines.

Listing Agreement

A listing agreement is a signed contract between you and your real estate agent that allows the agent to list your house for sale. For the lender, it is evidence that the property is being marketed actively, which is a vital condition for short sale approval.

An unequivocal listing agreement indicates the seller’s dedication to the completion of the transaction and also contains information such as the listing price, the duties of the agent, and the marketing plan, among other things.

Authorization Form

An authorization form enables your real estate agent to reach out to the lender directly on your account. Your agent will be able to submit the required paperwork, negotiate different terms, and do the necessary follow-ups, all of which can make the approval process faster.

Besides, lenders usually demand this as a sort of safeguard that they have the legal right to communicate about your finances with your agent.

Offer Evaluation

After a buyer has submitted an offer, lenders will review the offer to see if the sale price really represents the market value. They check the offer with the help of appraisals or comparative market analyses and also go over the terms, like contingencies, closing date, and deposit amount.

If the first offer is not the lender’s cup of tea, they can always discuss counteroffers. This is kind of a safety measure for a lender that ensures that the buyer will get a financially reasonable and fair deal.

Documentation of Past Payments

Mortgage lenders will often ask for documents that demonstrate both previous mortgage payments and the status of property taxes.

Through the former, they’ll be able to judge whether or not the current homeowner has been meeting the prior commitments, while the latter allows the lender to understand the entire situation for making a decision. Having precise and current records on hand can greatly help to accelerate the review procedure.

Updated Financial Information

Timescales for obtaining approvals of a short sale can be very different, some of them even lasting several weeks or months. During this period, if situations change, lenders are entitled to ask for updated financial documents.

Giving them updates in a timely manner is a way to move the process along without problems and also enhances the chances of getting the lender’s approval.

Take a look at this short sale paperwork checklist for further clarifications:

| Checklist Item | Description |

| Hardship Letter | Letter explaining financial hardship preventing mortgage payments. |

| Income Proof | Recent pay stubs, tax returns, and bank statements. |

| Monthly Expense Statement | Breakdown of household expenses. |

| Mortgage Statement | Latest statement showing remaining mortgage balance. |

| Net Sheet | Estimated sale price, costs, and expected lender shortfall. |

| CMA or Appraisal | Property valuation based on market comparables. |

| Listing Agreement | Signed contract with real estate agent to sell the property. |

| Authorization Form | Permission for the agent to communicate with the lender. |

| Purchase Offer | Buyer’s written offer with terms and price. |

| Payment History Records | Documents showing past mortgage payments and tax status. |

| Updated Financial Documents | Updated financial information if requested during review. |

Why Short Sale Timelines Are Longer Than a Standard Cash Close

When it comes to short sale vs cash offer Delaware, short sales are known to take longer than a normal cash purchase as there are more parties involved, and the transaction has to be approved several times. In a typical cash sale, the buyer immediately pays, and the deal closes very quickly. But in a short sale, you need the lender’s review and approval at various points.

First of all, for the lender approval short sale process, they has to judge the homeowner’s hardship. This means they have to see the hardship letters, check proof of income, monthly expenses, and other documents. Just collecting and sending this information to the lender can take a number of weeks. Then the lender does a full financial check, which means checking the net sheet, outstanding mortgage balances, and secondary liens.

They also have to make sure that the sale price is right for the house, so they ask for appraisals or comparative market analyses. Please note that if the home has different liens, each one has to give its consent to the sale. Trying to get responses from several lenders ends up taking more time.

If the review process is going on for many weeks or months, lenders will probably also ask for updated financial details. At the end of the day, the lender is also free to negotiate or ask for counteroffers to the buyer’s proposal, which continues to make the timeline longer. On the other hand, in a usual cash close, you do not require the lender’s approval, thus completing the transaction at a much faster pace.

Alternatives to a Short Sale

There are other options besides short sales for homeowners who are struggling with mortgage payments.

Firstly, one of these is a loan modification, a process through which the borrower and lender agree to change the mortgage terms. Such a change could be a reduction of the interest rate or an extension of the repayment period, resulting in lower monthly payments.

Secondly, another alternative is refinancing. When you refinance, you take out a new mortgage, preferably with a lower interest rate, to pay off the old one. A new mortgage with better terms can help to lower your monthly payments. Yet, if you are already late on payments, getting approved for refinancing may be quite difficult.

Thirdly, you can consider a deed in lieu of foreclosure. This means you essentially give up the home to the lender who, in exchange, helps you from the mortgage debt. Even though the deed in lieu will leave a mark on your credit report, the damage to your credit usually is less drastic than a foreclosure.

Conclusion

For homeowners who are having financial difficulties, doing a short sale is one of the options to secure themselves. But it usually takes time since lenders have to approve and give you a lot of documents.

Buyers who want to buy quickly can consider a cash buyer alternative to short sale that will make the whole process easier, resulting in faster closings, fewer problems, and still giving you the chance of buying and selling properties in an efficient way.

FAQs

Does a short sale always require lender approval?

Basically, a short sale is a discounted sale of property that requires a lender’s approval to go ahead.

Can I accept a cash offer while pursuing a short sale?

Certainly, accepting a cash offer is a great idea, the lender has to approve the short sale in order for the closing of the transaction.

Will a short sale stop foreclosure automatically?

Declaring a short sale does not stop foreclosure immediately; they must review it first to see if they might allow a temporary delay of the foreclosure to be signed off on.

What happens if the lender rejects the short sale?

If the lender rejects the short sale, the homeowner may get foreclosed upon or have to look for other options, such as a loan modification.

What is a preforeclosure short sale Delaware?

Preforeclosure short sale in Delaware is when a homeowner sells the house before it’s foreclosed, with the lender’s consent to reduce the mortgage loss.

What is a loss mitigation short sale?

A loss mitigation short sale is a lender-approved sale aimed at minimizing financial loss while assisting homeowners in avoiding full foreclosure.